First, the international market consolidation upward this month, the international steel market trend steady upward. After the end of the summer break in Europe, demand began to pick up. Traders and users gradually accepted price increases from steel mills. The high price of American sheet metal fell back, mainly due to the expected increase in supply, and the price of wire rods remained stable. The Asian market remained strong. Due to the continued devaluation of Southeast Asian countries and Indian currencies, the two regions of China’s steel exports were temporarily blocked. Korea, Japan, and other East Asian countries and regions performed well, and steel mills have raised prices. In general, the international steel market remains strong in the short term.

European market remains strong in Europe. In flat products, the European coil market remains strong. With the end of summer vacation in most Nordic countries, market transactions tend to be active. The price increase of coils announced by Nordic steel mills has been partially accepted by the market since July, and the increase in coil prices is relatively large. It is expected that the price will increase further in the later period. At present, the ex-works prices of hot-rolled coils for Nordic steel mills in the fourth quarter have been raised to 450-470 euros/tonne, but the German service center has not yet accepted the ex-factory price higher than 440 euros/tonne. Due to the competition of imported resources, the volume of cold-rolled coils rose less, and the current ex-factory price is about 540 euros/ton, and the price accepted by buyers is 520-525 euros/ton. In order to maintain this upward trend since July, European steel mills plan to continue raising prices. This week, ArcelorMittal once again announced an increase in coil prices, ex-works prices to 490 euros/ton, cold coils and hot-dip The ex-factory price of zinc coils was adjusted to 570 euros/ton, with an increase of 20-30 euros/ton. Affected by higher prices of imported European resources, it is expected that other European steel mills will follow the price increase.

In the North American market, the US thin plate weakened. The price of thin plates in the United States fell slightly this week, and the market transactions began to shrink. At present, the ex-factory price of hot coils in the Midwestern steel mills is 650-665 US dollars/short ton, which is 5-10 US dollars/short ton lower than before, and cold rolls are down 5 US$/short ton to 760-770 US$/short ton. Market participants said that most of the sales of hot rolled coils were still traded at about 660 US dollars/short ton. With the emergence of low-priced transactions, buyers began to be cautious, slowing down the pace of procurement, resulting in the main reason for the price decline is the market. Expected supply will increase. As for the decline of the market, the dominant steelmakers believe that it is only a short-term adjustment and there is still room for growth in the latter period. The steel mills stated that although AK Steel and American Steel are about to restart some equipment, some steel mills will stop production and maintenance, and there will be no obvious increase in market supply in the later period. The supply and demand in the later period can still maintain a balance. After a period of adjustment, the US thin plate. Prices will regain gains.

Asian markets have steadily increased in Asian markets. Flat material, to maintain stability. After the price of Chinese HRC exports to South Korea continued to rise, South Korea's importers delayed the signing of contracts. The stock of imported resources in South Korea was also rapidly depleted over the same period. It is estimated that most of the company's stocks will bottom out by the end of September. At present, the quotation of Chinese HRC exports to South Korea is US$570/tonne (CFR). In South Korea, steel mills have also raised their prices. Pohang and Hyundai Steel have raised HRC prices by 30,000 won/ton, and Eastern Steel has raised 40,000 won/ton. Taking into account the upcoming demand season and the low market inventories, Korean buyers are expected to gradually accept quotes from Chinese steel mills. In India, the recent devaluation of the Rupee has caused some Indian HRC producers to seek greater price increases for shipments in September, up by Rs 3,000/t (US$44/t). Affected by the devaluation of the rupee, the current domestic coil market price in India is about US$100/ton lower than that of the international market, and imported resources are no longer competitive. Despite this, India's domestic market demand is weak, and higher prices cannot be maintained until demand clearly rises. Market participants expect that steelmakers can only achieve part of their target increase, which is 1,500-1800 rupees/ton ($22-26/ton). At present, the average transaction price for hot rolled coils of 3mm thickness and above in India is Rmb3,4000-34,500/t (US$499-506/t), and the ex-factory price for large orders is Rs 33,500/t.

Second, the coated coil production and apparent consumption analysis According to my latest statistics of the steel network, July 13 production data fell back to high, the specific data are as follows:

The output of the plate in July was 3.533 million tons, a decrease of 8.47% from the previous period; it was a year-on-year increase of 6.77%. From January to July, a total of 24,322,000 tons of coated plates were produced in China. The output of coated plates in July was 610,000 tons, a decrease of 8.82% compared with the previous period, and a year-on-year decrease of 15.63%. From January to July, a total of 4.102 million tons of coated plates were produced in China.

The combined output and import and export data show that the apparent consumption of coated coils was as follows: The apparent consumption of galvanized coils in July was 3.241 million tons, a decrease of 307,900 tons from the previous month and an increase of 82,900 tons from the same period of last year; The nominal consumption of coils in July was 177,900 tons, a decrease of 117,000 tons from the previous month and a decrease of 197,600 tons from the same period of last year.

According to the latest customs statistics, the volume of galvanized coil imports in July was 114,200 tons, an increase of 10,500 tons over the previous month and an increase of 28,500 tons over the same period of last year; the export volume of galvanized coils in July was 433,100 tons. It decreased by 08,600 tons from the previous month and increased by 50,900 tons from the same period of last year.

According to the latest statistics from the Customs, Cai Tu’s imports amounted to 23,200 tons in July, a decrease of 0.3 million tons from the previous month and a decrease of 13,400 tons from the same period of last year; Cai Tu’s export volume in July was 457,300 tons, an increase of 5.5 from the previous month. Ten thousand tons, an increase of 56,000 tons over the same period of last year.

III. Analysis of price trend of zinc ingots My nonferrous metals report: The performance of the domestic zinc market continued to rise slightly this month, and the spot market for 0# zinc ingots maintained a high premium. The domestic spot 0 # zinc ingots offer range is 15000-15250 yuan / ton, 1 # zinc ingots offer range is 14900-15150 yuan / ton. The premium is 80 to 200 yuan/ton. The price of imported 0# zinc ingots is slightly lower at around 50-80 yuan/ton. However, the spot market volume tends to be light, in addition to the weak downstream demand, the tight supply of goods in the market and the strong price of the holders of the goods are also one of the main reasons for the low downstream willingness to accept goods.

At present, the funds of smelters are still not optimistic, and since this year's downstream procurement has been in a state of shrinkage, so the smelter to maintain a lower operating rate. This week, Luoping Zinc announced the sale of assets, Chihong Zinc, the inflated results of non-operating income and other negative news further confirmed that the degree of domestic smelter losses is extremely serious. Reducing production and reluctant sales as a means of price protection can only be seen in the short-to-medium term. In the long-term, it still lies in the expansion of end-use consumption to truly restore the value of zinc ingot itself. Therefore, we believe that when zinc prices return to profitable prices, the major smelters in the country will focus on releasing production capacity, and then will form resistance to the rise in zinc prices.

In summary, although the zinc price returned to above 15,200 yuan/ton this month, and exceeded the highest price since March 5, but only from the downstream purchase volume, there is no substantial reason to support the increase. The positive news or technical boost is not a rational rise. It is difficult for zinc prices to remain high until the peak season. Therefore, we believe that there will be a possible downward adjustment in zinc prices in the short term. It is recommended that the market be cautiously bullish.

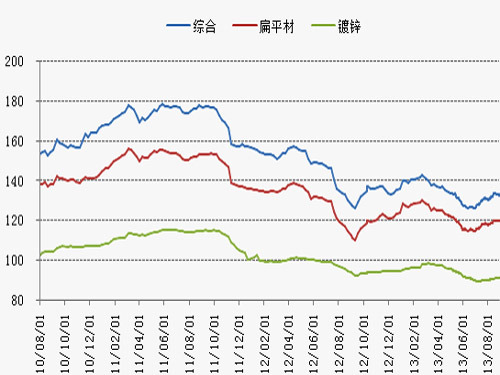

A brief review of the market in August and August (I) The Myspic price index changes according to the MyspiC price index (my steel price index is the abbreviation of MysteelpriceindicesofChina). As of the end of August 2013, the domestic steel price index was 132.8 points. It rose 1.38% from the previous month and rose 3.29% from the same period of last year. The price index for flat products was 119.77 points, which was an increase of 1.29% from the previous month and an increase of 6.30% from the same period of last year. The price index for galvanized coils was 91.37 points, which was an increase of 0.99% from the previous month and a decrease of 3.01% from the same period of last year.

(II) A review and outlook of market conditions in various regions in August 1. The market price of coating in the Yangtze River Delta region in eastern China rose slightly this month. By the end of the month, the prices of galvanized and coated products had risen by nearly RMB 30/ton from the beginning of the month. Demand appears to have a high middle-to-low trend at the end of the month. Fortunately, after the cost of steel mills rises, it gives businesses certain confidence in support. Although there is a wait-and-see mood, it is not strong. At present, the supply of steel products is not timely, resulting in the lack of market resources is also an important factor causing prices to rise; In addition, the gradual shift in the weather has also pulled some of the demand. For now, the short-term situation is still more ambiguous: 1. The increase in the price of steel mills is not willing to ship cheaply, the downstream businesses wait and see, the operating intention is relatively light; 2. The steelmaker expects to reduce the production in the later period and will increase the ex-factory price in disguise. Or it will lead to a period of inversion so that the market will not rise or fall. 3. Some steel mills will skip the intermediate circulation and move their resources forward. This will also bring certain sales pressure to the market and it will be difficult to emerge in the short term. One-on-one movements; 4. The recent export pressure of coated products has improved, but this can only play a mitigating role for the market; in the later period, the market fundamentals have not yet been effectively changed, and downstream demand will be gradually released. It is estimated that there will be a slow upward movement of prices in the later period.

The price of coated coils in the Boxing Market this month oscillated upwards. At the end of the month, most of the prices of the coated coils rose. Only a few specifications were slightly adjusted back. In terms of overall price performance, due to uneven demand structure, local galvanized coils have different performance in terms of regulatory resources: 0.17mm thick thin-gauge color substrates have fallen slightly under the premise of weak demand and fewer orders; The thickness of 0.23-0.5mm resources performed well and the increase was obvious. Relatively speaking, although the performance of thick-scale resources was repeated, it also rose slightly under the support of the price increase of leading steel mills in September. On the other hand, the price of upstream SPHC hot rolled coils is mostly consolidating, but due to the environmental factors in Hebei Province, the production capacity is still significantly suppressed, resulting in tight billet, hard rolling, etc., and the price rises upward. The settlement price of hot-rolled steel products eventually increased sharply, which further strengthened the production costs of local private enterprises. The SPHC3.0mm*1010-size hot-rolled coil volumes settled at RMB 3,730/ton, up RMB 100/ton from the previous month. In the next September, it will enter the peak demand season for thin sheet products. The market sales volume should be able to improve compared to August. At the same time, dealers are expected to be cautiously optimistic and stable. Based on the above factors, it is expected that the coating coiling in the Boxing market in September will be able to maintain upward momentum.

2. The coating prices in North China market in North China this month continued to pick up slightly from last month. The main reason is that the pricing policies of major steel mills in the country were basically adjusted to the tone in September, and the market merchants pulled up under the influence of cost support. The willingness of prices appears to be more intense; secondly, as of the end of August, this year's “summer break†has basically ended, and the so-called “golden nine silver ten†peak season will soon be ushered in, so business confidence in the market has also been significantly enhanced. In terms of galvanizing, as of press release, the mainstream transaction price of 1.0mm*1250mm*C in the market of Shougang Jingtang in Tianjin market was around 4,430 yuan/ton, up by 80 yuan/ton from the previous month; Beijing Shougang spent 4500 yuan/ton on flower resources in the market. It was increased by 50 yuan/ton from the previous month. In terms of color coating, as of the press release, the mainstream quotation of Xinyu 0.47*1000*C in Tianjin market was around 5,180 yuan/ton, and the price rose sharply by about 100 yuan/ton compared with the previous month. The offer price of Beijing-Tianjin color coating was basically the same. Steel price adjustments: The price of galvanized steel in the North China region and August this month remained stable at 4480 yuan/ton, but the ordering ratio was significantly different from the previous month, and the proportion of galvanized orders was only 65% ​​this month. It is understood that the main reason is that steel mills export orders are better, and secondly, domestic trade orders in September significantly improved from the previous month. This month, the color-coated private steel mills will continue to increase the factory guidance price. According to the author's understanding, Hebei Zhonggang’s 0.47mm is raised by RMB 100/ton; Xinyu has been raised by RMB 70/ton twice. In another development, according to the author's understanding, the large-scale private steel mill that had ceased production in previous years, China Metallurgical Hengtong, or will resume production in November this year, this time a total of four galvanized production lines will be re-produced, and it is expected that each month The output of the production line will reach 18-20,000 tons. If the news is true, I think this will inevitably affect the pattern of the galvanized market in North China. Overall, this month's galvanized overall stable operation, is expected to fluctuate slightly next month.

3. The coating market continued to increase in the south-central region of Central and South China. The price of galvanizing resources rose by RMB 100-150/ton, and the transaction volume was reduced. In terms of price, as of the press release, Wuhan Market Wuhan Iron and Steel galvanized 1.0*1250*c quoted at 4,650 yuan/ton, the same specification Egang, Yellowstone resources 4600-4650 yuan/ton, all-pass resource 4570 yuan/ton; color coating, Wuhan Iron and Steel 0.5 *1250*c quoted at 5,700 yuan/ton, same specification Baosteel Huangshi 6500, Hanke 0.4mm quoted at 5580 yuan/ton, Xinyu 0.42mm quoted at 5350 yuan/ton. In August, the hot-rolled varieties did not turn downwards even if they did not continue to rise. The coated products continued the upward trend of the market at the end of July. In September, Wuhan Iron & Steel raised its price by RMB 130/t without tax, resulting in an intermittent rise in the local plating market price. As of the end of the month, private enterprises in Huangshi District, galvanized coil .0mm mainstream offer 4520-4550 yuan / ton. In addition, compared with the previous month, market demand has dropped significantly, sales volume has dropped by about 20%, most of the merchants' inventory is at a low level, and the cycle of replenishment has been elongated and the quantity has decreased. The decrease in the order quantity of merchants, the tightness of hot-rolled raw materials of some specifications, and the high price have led to the current situation that the market is in a state with low resources, new resources, and incomplete specifications. Regarding the market outlook, taking into account the operation of the hot rolling market, Xiao Bian believes that the first half of the month basically runs smoothly, and as the market demand picks up, and the surrounding market resources circulate, the price gradually rises, and the market may usher in the second half of the month.

4. In South China this month, the plating coating market in South China has been consolidating upwards. The galvanized steel has soared. The color coating has been weaker than last month. Demand is generally satisfactory. Businesses are optimistic about the market outlook. In terms of price, Anshan Iron & Steel 1.0mm has a flower offer of 4,650 yuan / ton, Shougang 1.0mm no flower offer 4,680 yuan / ton, Tiantie 1.0mm no flower offer 4,580 yuan / ton, Wuhan Iron and Steel 1.0mm without flower reported 4,680 yuan / ton, Ma Gang 1.0mm without 120g zinc layer offer 5050 yuan / ton. In terms of color coating, Baosteel 0.5mm reported 7,500 yuan/ton, Arima 0.426mm reported 6,300 yuan/ton, Huamei's specifications were reported at 6,000 yuan/ton, Kilian's specifications were reported at 5,200 yuan/ton, and Nanhan's specifications were reported at 5300 yuan/ton. Ton. The South China market this month performed well in the first half of the month. The second half of the month was relatively weak due to rainy days and order repayments. For different varieties, the galvanized surface is better than the color coating. Galvanizing was affected by factors such as price increase by steel mills, and there were signs of rapid recovery in the middle of the month. The rebound rate was between 100 yuan/ton, which made China's prices faltered and was no longer the lowest in the country. In the latter part of the year, due to the reduction of orders from businesses, the market has reduced the amount of galvanized resources, and the specifications have been lacking, which has led to high prices for some resources. But there is a more stable galvanized flower. The color coating demand weakened this month. Local private manufacturers were forced to ease the pressure on shipment prices, and there was no significant adjustment. Individual manufacturers were forced to increase slightly due to cost pressure. The overall demand was generally lower. Relative to the previous month, the orders received by the manufacturers were relatively normal, and individual orders were significantly reduced. At the end of the month, there was a one-week or ten-day suspension of maintenance. In terms of demand, the terminal's production before November was relatively strong, supporting the market outlook. Coupled with the high cost and other factors, plating in South China is expected to move forward next month.

5. In the northeast region, the prices of plated coils in the northeastern market of this month have been consolidating upwards, and transactions are fair. Price: At present, Shenyang market 1.0mm Bengang Resources offer is 4,620 yuan / ton; Shandong developed 0.3mm quoted at 4,890 yuan / ton; Cai Tu, the Harbin market Xinyu 0.47 * 1000 * C quoted at 5,200 yuan / ton; Bazhou Jinghua 0.476*1000*C color coating resource quoted at 5,200 yuan / ton. At the beginning of the week, due to the shortage of local coating resources, the market has a clear “good price and high price†attitude. Merchants’ prices have increased slightly, and shipping conditions are still acceptable. In terms of galvanization: With the introduction of price adjustment policies by leading steelmakers such as Baosteel and Wuhan Iron and Steel in the middle of the week, the market is expecting a stronger price adjustment for local steel mills, and the mentality of pushing up is more obvious, but it is constrained by local downstream demand restrictions, which will increase the rate of increase. Limited; and in the introduction of a new round of price policy in the saddle, the market due to advance overdraft of the corresponding price range, so the mainstream stability, some pushed up 10-20 yuan / ton, shipping is limited. In terms of color coating, although the midweek steel companies such as Hebei Steel, Jinghua and Xinyu introduced a new round of price policies, the market has only slightly increased. At present, the out-of-stock situation of coated coils in the northeast region has eased compared to previous years. Supply and demand are relatively balanced, and the market price has been in a saturated position since the previous period. In addition, taking into account the National Games lasting nearly two weeks in early September, will affect downstream construction to a certain extent, and the recent macroeconomic side is also no good, is expected in the short term the local market plating prices may be narrower consolidation.

6. The cost of resource coating in the northwest region of the northwest region has been pushed up, and prices have continued to increase by 50-80 yuan/ton, and terminal demand has been weak. In terms of price, as of the press release, Xi’an Market 1.0*1250*c wine, galvanized steel price quoted at 4,630 yuan/ton, same specifications Huangshi Shanli, Shengye and Huaru 4580-4620 yuan/ton, Cai Tu, Fengyang, Xinyu 0.45 * 1000 * c offer 5150-5200 yuan / ton. In the August market, resources were mainly inventories in the early stage and a small number of new arrivals such as JISCO and Hualu. The specific situation was as follows: the cost of resource costs continued to increase, while the local market was lightly traded, and the cycle of merchant replenishment was significantly elongated. It seems that with Huang Shi and Jin Tang, these two major resources are cut off from each other. The market turnover can also reflect the weakening of demand, several medium-sized businesses shipped 500-1200 tons this month, some businesses said that end-users also face two major problems: the poor availability of funds and the new connection Less orders. In the color coating market, some steel companies have entered Xiaxiu for a period of time, and the outdoor high temperature has affected the construction. The amount of their projects is no more than that of the galvanized market. Regarding the market outlook, taking into account the operation of the hot rolling market, Xiao Bian believes that the first half of the month basically runs smoothly, and as the market demand picks up, and the surrounding market resources circulate, the price gradually rises, and the market may usher in the second half of the month.

7. In southwestern China this month, the low price of plating in the southwestern market continued to increase significantly, and the high level slowly picked up. The market demand gradually developed towards a healthy trend. It is understood that the current mainstream market price of galvanized 1.0mm is located between 4650-4700 yuan / ton, color coating 0.4mm mainstream quoted at 5250-5450 yuan / ton. Business feedback, due to the impact of high temperature weather, the market's demand for the first half of the month was poor, but as the high temperature weather gradually eased, the demand for steel coating in the second half of the month was gradually improved under the conditions of the project and construction started to improve. Most merchants shipped daily. The amount of 100 tons of pressure is gradually reduced. Relative to the gradual recovery of the market, the profitability of the steel mills has also improved. Manufacturers have followed the lead manufacturers to increase the price policy in September. It is understood that the local state-owned giant Panzhihua Steel Co The tax is raised by RMB 100/t. Meanwhile, based on the cost of hot-rolled C materials, the cost will increase by RMB 100/t. Private factories will also increase prices in early September. Businesses said that rising costs will inevitably promote the improvement of gold market conditions in September, but the market also said that when the size of the market gains may still be more based on the improvement in market demand. In terms of resources, early-stage merchants were slightly negative on August orders, and the market arrivals this month were generally low. In addition, the previous supply of private steel plate bases was insufficient, which also led to lower production and supply of Chongqing Wanda, Chongqing Longjin, and Sichuan Kaixi. The market must have out-of-specifications and stalls. Businesses believe that due to the prevailing market inventories are generally low, businesses are relatively lenient with handheld funds, and their willingness to open positions in September is likely to increase, which may drive up the price and passion of manufacturers and traders. In terms of production capacity, on the morning of August 6, Chongqing Fuyang Industrial Zone, Liangjiang New Area, Chongqing, Chongqing, China, started construction of the Angang Group’s Chongqing high-strength galvanized auto sheet project. This will have a greater impact on the high-end brand market in the southwest in the later period, and the market may pay more attention. In summary, the operating environment of the steel market has gained a lot of advantage, and it is expected that the market price for coating in the southwest is expected to continue to rise slightly.

V. Late-stage coating market or steadily rising After this month, the average price of coating market rose by 40 yuan/ton. Market prices across the country began to obviously improve to a certain extent. Based on the smelting policy adopted by most steel mills in September, the market will The cost of goods will further increase. In the face of August, the spot market price itself will not increase much faster than the previous August ** price increase. In addition to the new round of resource pressure on market prices in September, businesses may continue to push up market quotations to smooth out or May reduce market prices upside down. Business feedback, after the beginning of autumn, the high temperature has dropped significantly, driving the demand for construction steel and other steel. At the same time, the production of the factory has also shown significant improvement. The market demand for steel plating is expected to gradually improve. In addition, in the early July and August, the resources held by the merchants were relatively insufficient, and the market inventory was at a low level. The lack of stockholders reluctant to sell mentality or high price hanging discs; at the same time, the pre-rolled hot rolled steel C material increased significantly, privately-owned manufacturers lack of material preparation, which has intensified The relative lack of production of private enterprises, which give the market greater help from the supply. Therefore, the contradiction between supply and demand in the domestic coating market in September has eased, while the market's main players are in a strong state of mind. I expect the nation's steel coating market will increase its rationality.

HEUI tools are specially for HEUI diesel injection system repair, used for CAT C7, C9, C-9, 3126, and HEUI pump. These tools cover disassembly and assembly, measuring device, adaptors for different injectors etc.

These tools meet different maintenance applications, are easy to use, and greatly improve maintenance efficiency.

Heui Tools,Cat Heui Injector Repair Tools,Heui Injector Tools,Tools For Heui Injector Assembly

CHENGDU UNICO MACHINERY CO., LTD , https://www.injectortestbench.com